up:: 061e MOC Teorias Econômicas

related:: Questões P1 Macroeconomia B 1.2025

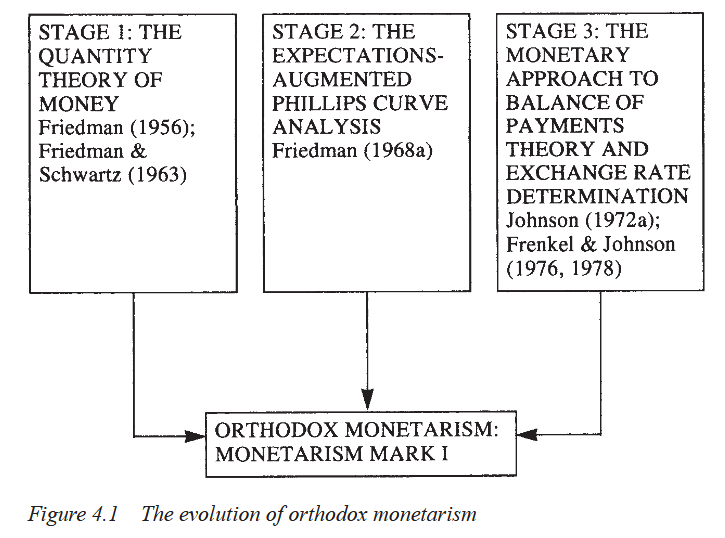

Fonte: SNOWDON & VANE, p. 164.

“In retrospect we can now see that Friedman’s debate with his critics demonstrated that their differences were more quantitative than qualitative, and contributed towards an emerging synthesis of monetarist and Keynesian ideas. This emerging synthesis, or theoretical accord, was to establish that the Keynesian-dominated macroeconomics of the 1950s had understated (but not neglected) the importance of monetary impulses in generating economic instability” (SNOWDON & VANE, p. 174; grifo meu)

Teoria Quantitativa da Moeda

Milton Friedman advoga que a demanda por moeda é como a demanda de qualquer ativo, sendo algo da forma

onde

Neutralidade da Moeda (a longo prazo)

A Não-Neutralidade da Moeda que aparece após uma Política Monetária, a curto prazo, se dá devido a expectativas de Inflação.

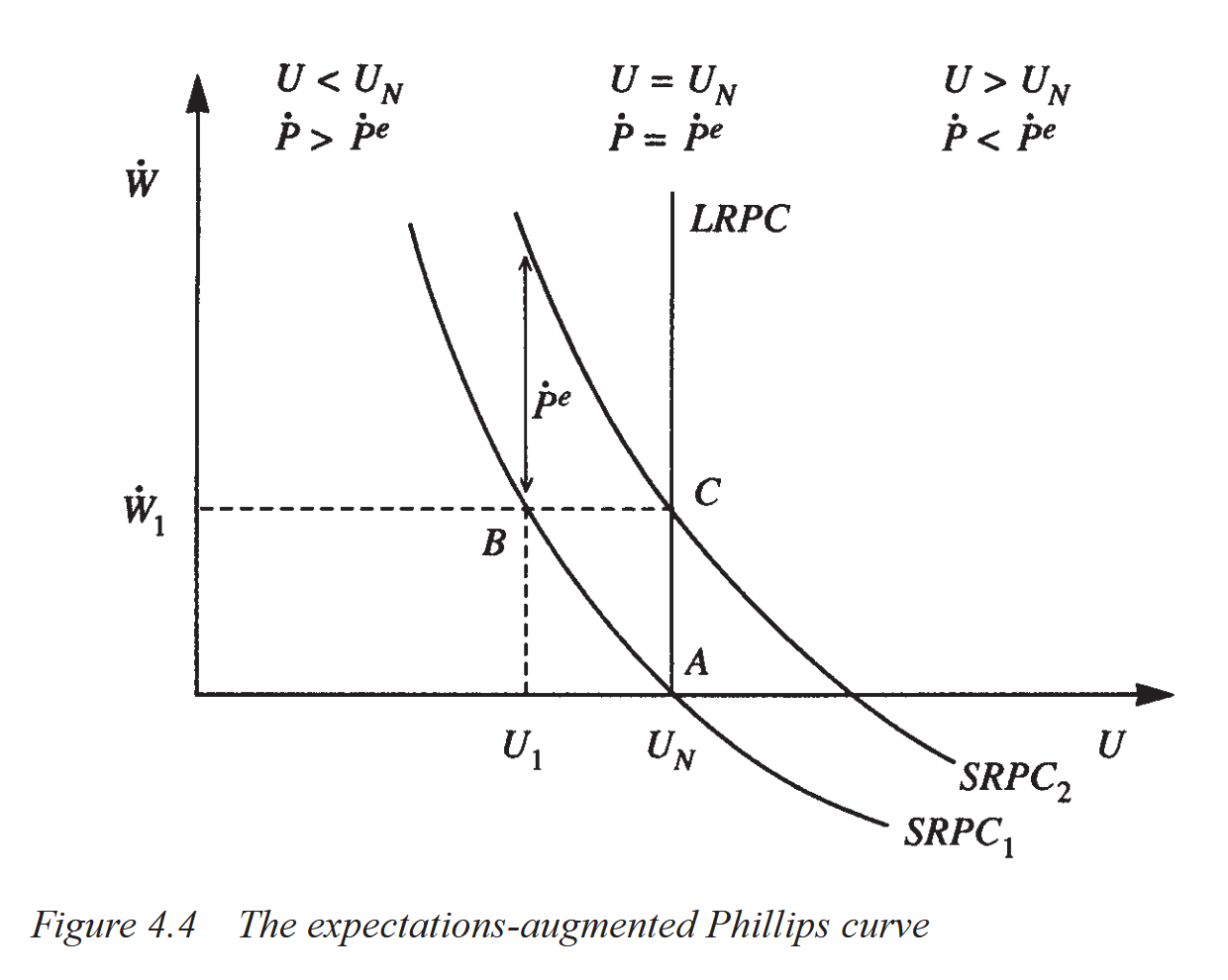

“…there is always a temporary trade-off between inflation and unemployment; there is no permanent trade-off. The temporary trade-off comes not from inflation per se, but from unanticipated inflation, which generally means, from a rising rate of inflation. The widespread belief that there is a permanent trade-off is a sophisticated version of the confusion between “high” and “rising” that we all recognize in simpler forms. A rising rate of inflation may reduce unemployment, a high rate will not.” (FRIEDMAN, 1968, p. 11; grifo meu)

Suponha-se uma Política Monetária Expansionista (cf. FRIEDMAN, pp. 9-11): surge um excedente de moeda, que os indivíduos — pela TQM que Friedman advoga, vide acima — buscaram cambiar por outros ativos; nesse fazer, diminuem a Taxa de Juros, além de aumentar o Consumo e Investimento. Portanto, haverá aumento de Produto Agregado, e Salários nominais aumentarão no processo, induzindo diminuição da Taxa de Desemprego.

Porém, os preços dos produtos de mercado aumentarão, devido à maior demanda, mais rápido do que preços de Fatores de Produção. Portanto, o nível geral de preços

“Indeed, the simultaneous fall ex post in real wages to employers and rise ex ante in real wages to employees is what enabled employment to increase. But the decline ex post in real wages will soon come to affect anticipations. Employees will start to reckon on rising prices of the things they buy and to demand higher nominal wages for the future.” (FRIEDMAN, p. 10)

Conforme há uma demanda maior por salários nominais, de forma a compensar a inflação esperada

Curva de Phillips Aceleracionista (distinguir curva aceleracionista de curva Phelps-Friedman (?))

Fonte: SNOWDON & VANE, p. 177.

Críticas a políticas de fine-tuning

Regras, não discrição

“My own prescription is still that the monetary authority go all the way in avoiding such swings by adopting publicly the policy of achieving a steady rate of growth in a specified monetary total. The precise rate of growth, like the precise monetary total, is less important than the adoption of some stated and known rate. I myself have argued for a rate that would on the average achieve rough stability in the level of prices of final products (…). But it would be better to have a fixed rate that would on the average produce moderate inflation or moderate deflation, provided it was steady, than to suffer the wide and erratic perturbations we have experienced.” (FRIEDMAN, 1968, p. 16; grifo meu)

References

- SNOWDON, Brian; VANE, Howard R. Modern Macroeconomics: Its Origins, Development and Current State. Edward Elgar Publishing, 2005.

- FRIEDMAN, Milton. The Role of Monetary Policy. American Economic Review, v. LVIII, n. 1, 1968.